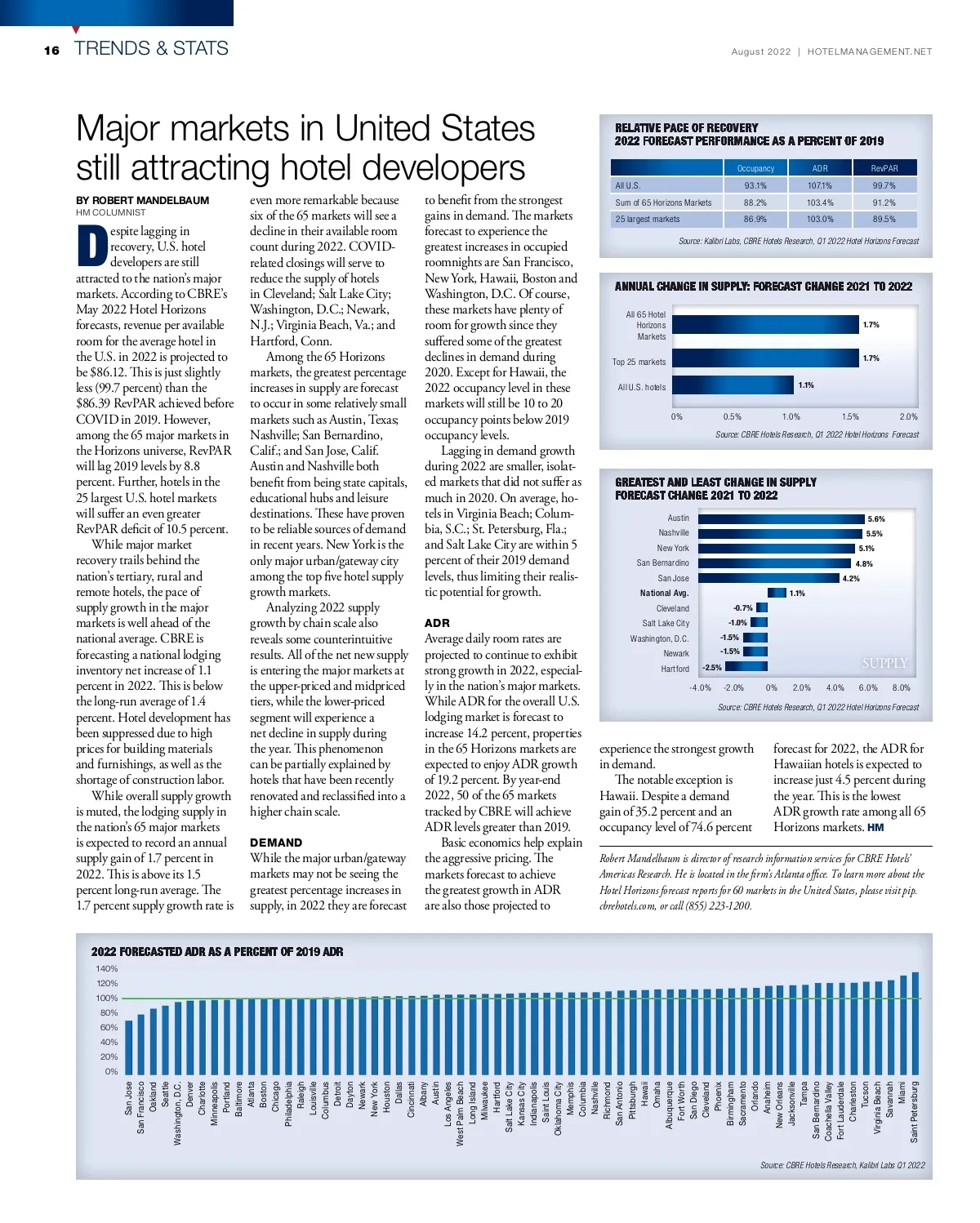

16 TRENDS & STATS August 2022 | HOTELMANAGEMENT.NET Major markets in United States still attracting hotel developers BY ROBERT MANDELBAUM HM COLUMNIST Occupancy All U.S. Sum of 65 Horizons Markets 25 largest markets 93.1% 88.2% 86.9% ADR 107.1% 103.4% 103.0% RevPAR 99.7% 91.2% 89.5% espite lagging in recovery, U.S. hotel developers are still attracted to the nation’s major markets. According to CBRE’s May 2022 Hotel Horizons forecasts, revenue per available room for the average hotel in the U.S. in 2022 is projected to be $86.12. is is just slightly less (99.7 percent) than the $86.39 RevPAR achieved before COVID in 2019. However, among the 65 major markets in the Horizons universe, RevPAR will lag 2019 levels by 8.8 percent. Further, hotels in the 25 largest U.S. hotel markets will su er an even greater RevPAR de cit of 10.5 percent. While major market recovery trails behind the nation’s tertiary, rural and remote hotels, the pace of supply growth in the major markets is well ahead of the national average. CBRE is forecasting a national lodging inventory net increase of 1.1 percent in 2022. is is below the long-run average of 1.4 percent. Hotel development has been suppressed due to high prices for building materials and furnishings, as well as the shortage of construction labor. While overall supply growth is muted, the lodging supply in the nation’s 65 major markets is expected to record an annual supply gain of 1.7 percent in 2022. is is above its 1.5 percent long-run average. e 1.7 percent supply growth rate is D even more remarkable because six of the 65 markets will see a decline in their available room count during 2022. COVID-related closings will serve to reduce the supply of hotels in Cleveland; Salt Lake City; Washington, D.C.; Newark, N.J.; Virginia Beach, Va.; and Hartford, Conn. Among the 65 Horizons markets, the greatest percentage increases in supply are forecast to occur in some relatively small markets such as Austin, Texas; Nashville; San Bernardino, Calif.; and San Jose, Calif. Austin and Nashville both bene t from being state capitals, educational hubs and leisure destinations. ese have proven to be reliable sources of demand in recent years. New York is the only major urban/gateway city among the top ve hotel supply growth markets. Analyzing 2022 supply growth by chain scale also reveals some counterintuitive results. All of the net new supply is entering the major markets at the upper-priced and midpriced tiers, while the lower-priced segment will experience a net decline in supply during the year. is phenomenon can be partially explained by hotels that have been recently renovated and reclassi ed into a higher chain scale. DEMAND to bene t from the strongest gains in demand. e markets forecast to experience the greatest increases in occupied roomnights are San Francisco, New York, Hawaii, Boston and Washington, D.C. Of course, these markets have plenty of room for growth since they su ered some of the greatest declines in demand during 2020. Except for Hawaii, the 2022 occupancy level in these markets will still be 10 to 20 occupancy points below 2019 occupancy levels. Lagging in demand growth during 2022 are smaller, isolat-ed markets that did not su er as much in 2020. On average, ho-tels in Virginia Beach; Colum-bia, S.C.; St. Petersburg, Fla.; and Salt Lake City are within 5 percent of their 2019 demand levels, thus limiting their realis-tic potential for growth. ADR Source: Kalibri Labs, CBRE Hotels Research, Q1 2022 Hotel Horizons Forecast All 65 Hotel Horizons Markets Top 25 markets All U.S. hotels 0% 0.5% 1.1% 1.7% 1.7% 1.0% 1.5% 2.0% Source: CBRE Hotels Research, Q1 2022 Hotel Horizons Forecast Austin Nashville New York San Bernardino San Jose National Avg. Cleveland Salt Lake City Washington, D.C. Newark Hartford -0.7% -1.0% -1.5% -1.5% -2.5% 1.1% 5.6% 5.5% 5.1% 4.8% 4.2% While the major urban/gateway markets may not be seeing the greatest percentage increases in supply, in 2022 they are forecast Average daily room rates are projected to continue to exhibit strong growth in 2022, especial-ly in the nation’s major markets. While ADR for the overall U.S. lodging market is forecast to increase 14.2 percent, properties in the 65 Horizons markets are expected to enjoy ADR growth of 19.2 percent. By year-end 2022, 50 of the 65 markets tracked by CBRE will achieve ADR levels greater than 2019. Basic economics help explain the aggressive pricing. e markets forecast to achieve the greatest growth in ADR are also those projected to SUPPLY 0% 2.0% 4.0% 6.0% 8.0% -4.0% -2.0% Source: CBRE Hotels Research, Q1 2022 Hotel Horizons Forecast experience the strongest growth in demand. e notable exception is Hawaii. Despite a demand gain of 35.2 percent and an occupancy level of 74.6 percent forecast for 2022, the ADR for Hawaiian hotels is expected to increase just 4.5 percent during the year. is is the lowest ADR growth rate among all 65 Horizons markets. HM Robert Mandelbaum is director of research information services for CBRE Hotels’ Americas Research. He is located in the rm’s Atlanta o ce. To learn more about the Hotel Horizons forecast reports for 60 markets in the United States, please visit pip. cbrehotels.com, or call (855) 223-1200. 140% 120% 100% 80% 60% 40% 20% 0% San Jose San Francisco Oakland Seattle Washington, D.C. Denver Charlotte Minneapolis Portland Baltimore Atlanta Boston Chicago Philadelphia Raleigh Louisville Columbus Detroit Dayton Newark New York Houston Dallas Cincinnati Albany Austin Los Angeles West Palm Beach Long Island Milwaukee Hartford Salt Lake City Kansas City Indianapolis Saint Louis Oklahoma City Memphis Columbia Nashville Richmond San Antonio Pittsburgh Hawaii Omaha Albuquerque Fort Worth San Diego Cleveland Phoenix Birmingham Sacramento Orlando Anaheim New Orleans Jacksonville Tampa San Bernardino Coachella Valley Fort Lauderdale Charleston Tucson Virginia Beach Savannah Miami Saint Petersburg Source: CBRE Hotels Research, Kalibri Labs Q1 2022

Hotel Management Hotel Management August 2022: Page 16